I Claimed $9M in Cost Reduction. My CFO Claimed I Was Wrong. We Were Both Right.

By Milind Tailor, Senior Procurement Leader

With an expert contribution from Sheldon Mydat, Founder & CEO, Suppeco

The $9M Conversation , And Why It Went Wrong

End of year QBR. Global IT. $90 million Annual Operating Plan on external spend.

I walked in proud. Seven major contracts renegotiated. Hardware unit costs down 6%. Payment terms extended with two strategic suppliers. Total claimed cost reductions: $9 million. The work was real. My team had delivered this.

“Then why did we exceed the AOP by $3 million?”

The CFO looked up and asked one question. I had no answer.

Because I had measured what I negotiated. He measured what the business spent. And nobody had built a bridge between the two. That moment changed everything about how I think about procurement. And it is what I want to talk about here.

Fluent in Procurement , Illiterate in Finance

Cost reduction is a procurement metric. Margin is a business metric. They are not the same thing.

CFOs live in Gross Margin, EBITDA, and Working Capital. Cost reduction does not appear as a line item on the P&L. It never did. Cost avoidance is worse still: ghost money. It never existed on the P&L, so it can never improve it. Every time I reported savings to Finance, I was speaking a language they did not use, about a number they could not find.

I have come to understand this the hard way: margin is not a destination. It is a living number, constantly being built up and eroded simultaneously. Procurement’s job is to be on both sides of that equation. For most of my career I was only on one side, and calling it enough.

The question my CFO asked every quarter was simpler and more brutal than any framework I had built: What happened to our margin, and why? My reporting answered 20% of that question. The other 80% was happening in plain sight.

Before I could point anywhere external, I had to confront something closer to home.

The Realisation Gap , I Was Claiming Dollars I Hadn’t Delivered

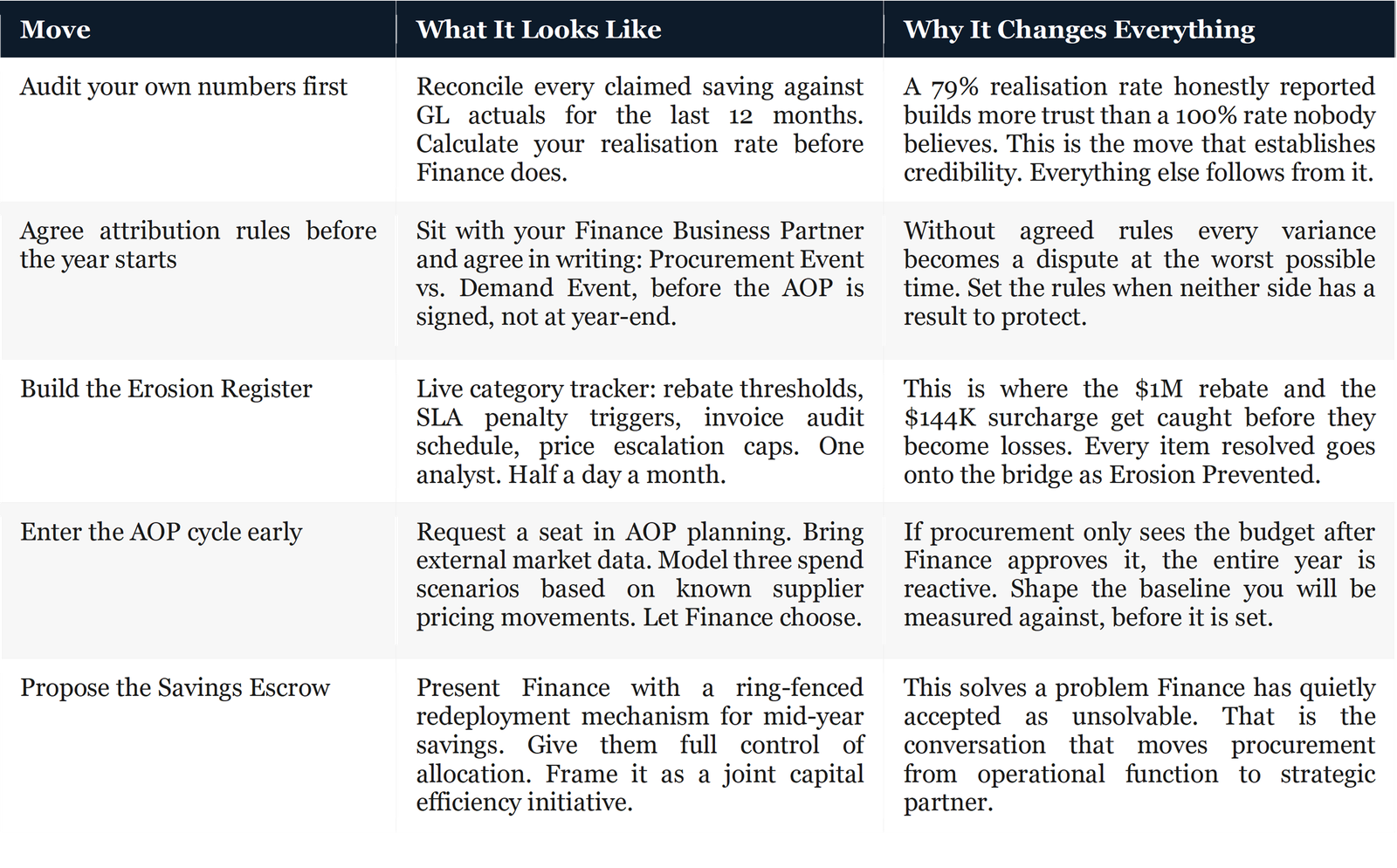

After that meeting I did something, I had never done in my career: I pulled up our claimed savings and reconciled them against what the GL actually showed, category by category.

What I found was uncomfortable. Across twelve contracts I reviewed that year, our average realisation rate was 79 cents on every dollar claimed. We were reporting $9 million in cost reductions. We had delivered closer to $7.11 million. The gap was not fraud. It was the consequence of measuring at the point of negotiation rather than the point of consumption.

Volume commitments used to secure better pricing – not met. Specifications changed post-contract – nobody repriced. Business units buying outside the agreement because the contracted supplier had a six-week lead time – flagged only at the year-end audit.

The bridge I needed to build with Finance could not rest on unverified numbers. Reconciling claimed against realised savings – category by category – was the foundation everything else had to stand on. That single discipline changed every conversation I had with Finance from that point forward.

The Leaking Bucket , Dynamic Margin Erosion in Reality

You negotiated a great price. Then the business lost it – slowly, quietly, in ways that never appeared on a single report.

Once I fixed my own numbers I saw the bigger problem for the first time. Sheldon Mydat calls this Dynamic Margin Erosion: the systematic leakage of value that occurs after the negotiation is complete. In the space between the contract and the invoice. The SLA and the scorecard. The rebate clause and the year-end claim.

I had been filling the bucket every year. Walking away. Calling it excellence. Here is what it actually looked like – starting small, and getting harder to excuse.

The invoice nobody audited , $144,000. A chemicals supplier billing a fuel surcharge that contractually expired eight months prior. AP auto-approved it every month because the PO matched. $18,000 a month. Eight months. Recovered, but only because one analyst ran a routine reconciliation. I had assumed Finance was catching this. Finance assumed we were. Nobody was.

The rebate nobody claimed , $1,000,000. A global logistics contract. $1 million annual rebate triggered at $50 million spend. We spent $53 million. Claim window: 90 days post year-end. No threshold tracker. No alert. No process. One million dollars of contractual entitlement – gone. Not because the contract failed. Because nobody owned the lifecycle between signature and claim.

The penalty we chose not to enforce , $500,000. This one is different. The first two were process failures. This was a decision, and the most honest thing I can tell you about how margin really disappears.

IT outsourcing contract. 99.9% uptime SLA. The provider averaged 97.7% for ten months. Penalty provisions: $50,000 per month. Amount claimed: zero.

“We know performance has been below target. But we are mid-negotiation on the next cycle and need this relationship to stay constructive.”

Two days before the QBR the supplier’s account director called directly. The operations lead agreed. The penalties were dropped. I signed off on it.

I call this the Relationship Hostage problem. The commercial right existed. The will to exercise it did not. Procurement negotiates the clause. The relationship team decides whether to use it. In that gap, $500,000 disappeared – and appeared on no report I ever produced.

Until commercial governance is structurally separated from relationship management, every penalty clause is optional in practice. The contract says otherwise. The behaviour does not.

Why did all three go undetected?

Three-way matching – Purchase Order, Goods Receipt, Invoice – is universally trusted as the gold standard of spend control. It validates quantity and PO price. Nothing else. It does not check whether the PO price matches the contracted price. It does not flag the expired surcharge, track the rebate threshold, or apply SLA deductions.

Three-way matching tells you the invoice is internally consistent. It tells you nothing about whether it is contractually correct. These are entirely different questions, and I had treated them as one for years.

The bucket does not leak because the contract is weak. It leaks because nobody is watching the seams – the joins between procurement, Finance, AP, and operations where value quietly escapes.

Invisible Erosion , Static Contracts versus Dynamic Delivery Interplay

A contribution from Sheldon Mydat, Founder & CEO, Suppeco

The three scenarios above – the phantom surcharge, the unclaimed rebate, the unenforced penalty – are patterns I have seen repeated across organisations of every size and sector, including defence, financial services, logistics, and public safety.

Every one of them comes back to the same root cause. The commercial agreement is static. The relationship is not.

A contract, an SLA, a scorecard, a rebate threshold. These are artefacts. They describe the relationship on the day it was negotiated. The relationship itself runs every day after that, and the gap between those two states is where Dynamic Margin Erosion actually lives.

Milind’s Relationship Hostage scenario is the cleanest example I have seen written down. The contract said one thing. The relationship said another. The penalty clause was static, sitting in the MSA, fully enforceable. The decision not to enforce it was dynamic, built over weeks of soft commitments and shifting tone that no governance forum had visibility of until the $500,000 was already gone.

This is the blind spot conventional reporting cannot close. KPI scorecards are the relational equivalent of three-way matching: internally consistent, contractually silent. They tell you whether the supplier hit their numbers. They tell you nothing about whether the commercial entitlement underneath those numbers is still being honoured, or quietly traded away in the operational layer where Finance never looks.

Closing that blind spot is not a reporting problem. It cannot be solved by adding another system of record, because more static data is what created the gap in the first place. It is a correlation problem.

The relationship between buyer and supplier generates a continuous stream of operational signal: communications, escalations, commitments made and missed, the texture of how the account is actually being run. That signal layer is where divergence from contracted reality first becomes visible. Suppeco’s proprietary relationship layer captures this dataset. SuppEQ analyses across it, correlating against the contracted state to surface drift months before it reaches the GL.

Milind’s three scenarios were all caught at year-end. Every one of them was visible months earlier in the relationship layer. That is the bucket nobody is watching.

The bucket doesn’t leak because the contract is weak. It leaks because nobody owns the seams

The Value Bridge , The Slide That Made $7.11M Impossible to Ignore

Twelve months after that first QBR I walked back into the same room with a different slide. Here is exactly what was on it.

That $0.63M favourable variance at the bottom is not a rounding error. It is my team delivering $7.11M of margin contribution against a $6.48M wave of business-driven demand growth, and finishing the year under budget. Without the bridge, my CFO saw a near-flat P&L and assumed nothing had happened. With it, he could see exactly what procurement delivered, what the business consumed, and precisely why those are two different numbers.

One rule I now hold without exception: when my team reduced laptop purchases from 2,000 to 1,500 units through an asset life extension programme, that $600,000 went on the Margin Enhancement line. Direct P&L impact. Not theoretical. Not avoidance. When an unrelated SaaS increase offset it the same quarter, I showed both as separate lines. I never net them silently. Silence is exactly how procurement becomes invisible.

The Savings Bonfire , Finance Knows It Happens, Nobody Stops It

Here is the problem nobody talks about after the bridge is built.

When procurement delivers savings mid-year, departments face a structural incentive to spend the surplus before year-end or lose it from next year’s budget. The saving is real. The redeployment is irrational. I have watched this happen with my own recoveries – a $400,000 reduction in a software contract, quietly absorbed into discretionary project spend by October, before I had built any mechanism to protect it.

Finance has accepted this dynamic because it has never been offered a structural alternative. That is procurement’s opening.

The fix is a Savings Escrow – mid-year procurement savings quarantined in a ring-fenced redeployment pool, not returned to the department, not surrendered to Finance’s general reserve, but allocated to pre-agreed growth initiatives. Procurement identifies the saving. Finance controls the redeployment. Neither side burns it unilaterally. This is not a complex mechanism. It is a trust mechanism – and procurement is uniquely positioned to propose it because it sits at the intersection of both problems. When you bring Finance a solution to a problem it has quietly accepted as unsolvable, the relationship changes.

Don’t Ask for a Seat , Make Yourself Impossible to Exclude

When you show Finance the bridge, you stop being an operational cost centre. You become a margin function.

Two things no table can fully capture.

Two things no table can fully capture.

Get Finance to co-sign the Value Bridge before every QBR – not to review it, but to validate the demand event classification and put their name on the slide. A bridge Finance helped build cannot be challenged by Finance in the room. That co-authorship is not a reporting tactic. It is a relationship transformation.

Hold a monthly Margin Governance Forum , 60 minutes, fixed attendees: you, Finance Business Partner, one operational lead. Agenda: realisation review, erosion register update, demand event sign-off, bridge update. Make Finance co-chair it. Their meeting. Their numbers. Their trust. Over twelve months, this single forum will do more for procurement’s strategic standing than any technology investment or organisational redesign.

One Year Later , The CFO Said Something I Didn’t Expect

I walked back in with the bridge slide. I walked him through $7.11 million in procurement contribution, line by line. I showed the demand events separately and explained why they were business decisions, not procurement failures. I showed him the Savings Escrow proposal for the coming year.

He did not say we had done a great job.

“This is the first time I have understood what your team actually does.”

Not praise. Something better – comprehension. And from comprehension comes trust, scope, and eventually the kind of strategic partnership that procurement has been trying to earn through better negotiations for decades. It was never about the negotiation. It was always about the bridge.

My CFO was not wrong that first day. Neither was I. We were looking at different parts of the same story, and I had never understood that connecting them was my job. It is. It always was.

Most procurement teams are one reporting change away from being the most strategically valuable function in the building. The question is not whether you are delivering value. The question is whether Finance can see it.

Can they?

What does your savings reporting look like today, and has Finance ever co-signed your numbers? Drop it in the comments.

About the Authors

Milind Tailor is a senior procurement leader with 20+ years of experience, focused on repositioning procurement as a margin function rather than a cost centre.

Sheldon Mydat is the Founder & CEO of Suppeco (suppeco.com), an AI powered Supplier Relationship Management platform recognised by IDC as a 2023 Named Innovator. Sheldon is also a 25 year practitioner having led supplier transformation programmes across defence, financial services, logistics, and public sector.